Articles

A Lending Bot That Wants You to "Transfer Your Coins" — How Does It Differ from a Legitimate Service?

Someone tells you "this lending bot guarantees X% monthly; just transfer your coins over and we'll trade for you" — that's the moment to raise the alarm. Real lending automation is "API-authorized, principal stays in your account"; one that wants you to "transfer your coins" to hold is structurally the same as a Ponzi scheme. Here are four red lines to tell real automation from a custodial pitch at a glance.

2026-06-13

Bear Market, Scared to Buy? Your Idle USDT Can Still Earn: Stablecoin Lending in a Downturn

In a bear or sideways market, you don't want to chase highs or catch a falling knife, so your USDT just sits idle. Stablecoin lending is a low-volatility option here: it doesn't bet on price direction, it just earns lending interest. But honestly: bear-market lending rates are usually lower too (less financing demand), and it isn't risk-free. This explains why a downturn suits lending, what rates look like, and what to watch.

2026-06-13

Can Lending Interest Cover Your Living Costs? A Drawdown Strategy for Monthly Cash Flow

Lending interest accrues almost daily, so in theory you can plan it as a monthly cash flow. But 'interest as living costs' requires thinking through three things: the rate is variable (monthly income changes), withdrawing sacrifices compounding, and never tap principal in low-rate months. This gives you a framework to turn lending yield into a steadier monthly cash flow — and how it differs from an 'accumulation' strategy.

2026-06-13

Year-End Bonus Earning Just 1.5% in a Deposit? A Plan for Idle Cash into USD Passive Income

A year-end bonus, an exit profit, or any sudden idle cash often earns just ~1.5% in a bank deposit while inflation nibbles at it. This explains a middle path: convert part of that idle cash into a USD stablecoin and lend it for USD-denominated variable interest. The point is how to allocate and control risk — not going all in.

2026-06-13

When Your Currency Keeps Falling: Hedging Inflation with USD Stablecoin Lending

When your local currency keeps depreciating, cash loses purchasing power and local fixed deposits can't keep up. One option is converting funds into a USD-pegged stablecoin (USDT/USDC) and lending it on an exchange like Bitfinex to earn USD-denominated interest. This explains exactly what it hedges, what it doesn't, and the risks you must accept.

2026-06-13

Still Trust an Exchange After FTX? A Full Breakdown of Lending-Bot Custody Risk

FTX scared a lot of people: hand your money to someone to hold, and they might misuse it. But lending-bot risk has two layers — whether the bot itself is non-custodial (can it touch your principal?) and the exchange's own counterparty risk are two different things. This explains the difference between "transfer your coins to us" and "just authorize an API," and which risk non-custodial removes versus which it can't.

2026-06-13

Rates Spiked to 25% at 3 AM, Gone by Morning: Why Manual Lending Always Misses the High Rates

Missing high lending rates isn't about judgment — it's physically impossible by hand. Rate spikes hit at random hours (often the middle of the night), last only minutes, and require you to post an order within seconds to catch them. You can't watch the market 24/7, but a bot can check every minute. Here's why the high rates always appear while you sleep, and what automation actually wins back for you.

2026-06-13

How Lending Bot Fees Work: Subscription vs Profit-Share, Which Is Cheaper for You?

Lending-bot fees come in three main shapes: subscription (fixed monthly fee), profit-share (a cut of what you earn), and tiered fee + overage cut. Which is cheaper depends on capital size and market conditions: large capital with high returns favors subscription (the fee gets diluted); small capital or bear markets favor profit-share/cut. This guide shows how to compare fees as a % of annualized return, not just the monthly number. EarnUSD uses a subscription with no cut — whatever you earn is yours.

2026-06-11

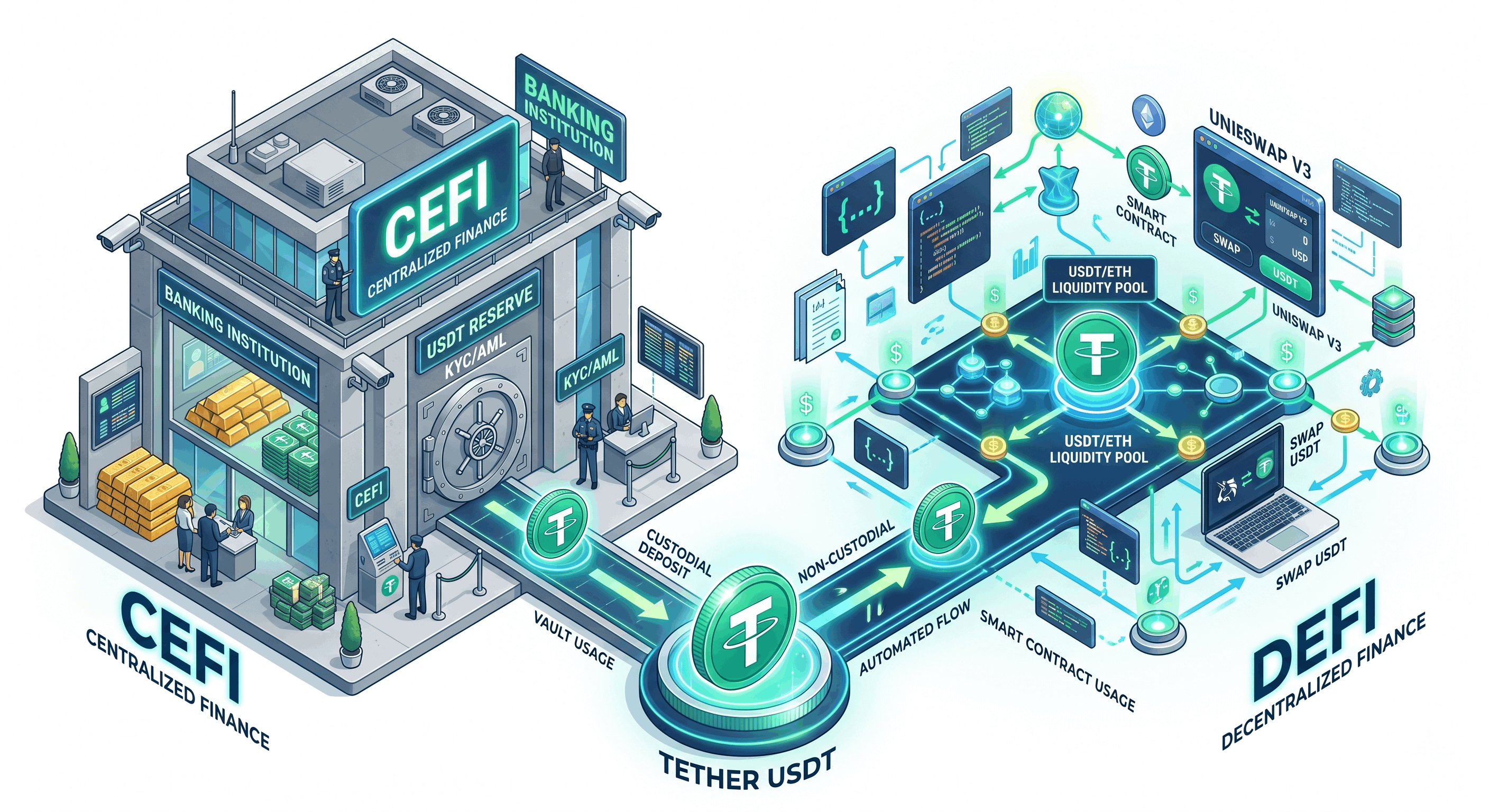

Bitfinex Lending vs DeFi (Aave/Lido): How to Choose for USDT Yield

To earn passive yield on USDT, CeFi lending (Bitfinex funding) and DeFi (Aave lending, Lido staking) are two paths with completely different risk profiles. The difference isn't who pays more (both float) — it's smart-contract risk vs exchange risk, the learning curve, and whose hands your money is in. This guide uses a table to clarify, and explains how two kinds of 'non-custodial' differ. For simple USDT interest without learning on-chain ops, exchange lending is usually easier, and EarnUSD can auto-grab high rates.

2026-06-11

Bitfinex Earn vs Funding (Lending): Two Kinds of Passive Yield Explained

There are two main ways to earn passive yield on Bitfinex — funding (lending) and staking — and they work completely differently. Funding means lending your USD/USDT/BTC to leveraged traders for floating interest; staking means locking specific PoS coins for protocol rewards. This guide uses a comparison table to clarify the assets, yield source, liquidity and risk of each. For stablecoins with flexibility, funding is usually more intuitive — and EarnUSD can auto-grab high rates for you.

2026-06-11