Bitfinex lending isn't depositing money into a pool — it's a peer-to-peer funding order book. You (the lender) post a funding offer (how much to lend, at what rate, for how many days), and margin traders (the borrowers) take your funds from the order book. The matching rule has one core principle: rate priority — the lowest-rate offers get filled first. Offer too high and your money sits idle earning nothing; offer too low and you leave money on the table. That dynamic is exactly why lending bots exist.

This 3-minute guide covers how the Bitfinex funding order book works, who the borrowers are, how matching is ordered, what role FRR plays, and why understanding this mechanism helps you earn more.

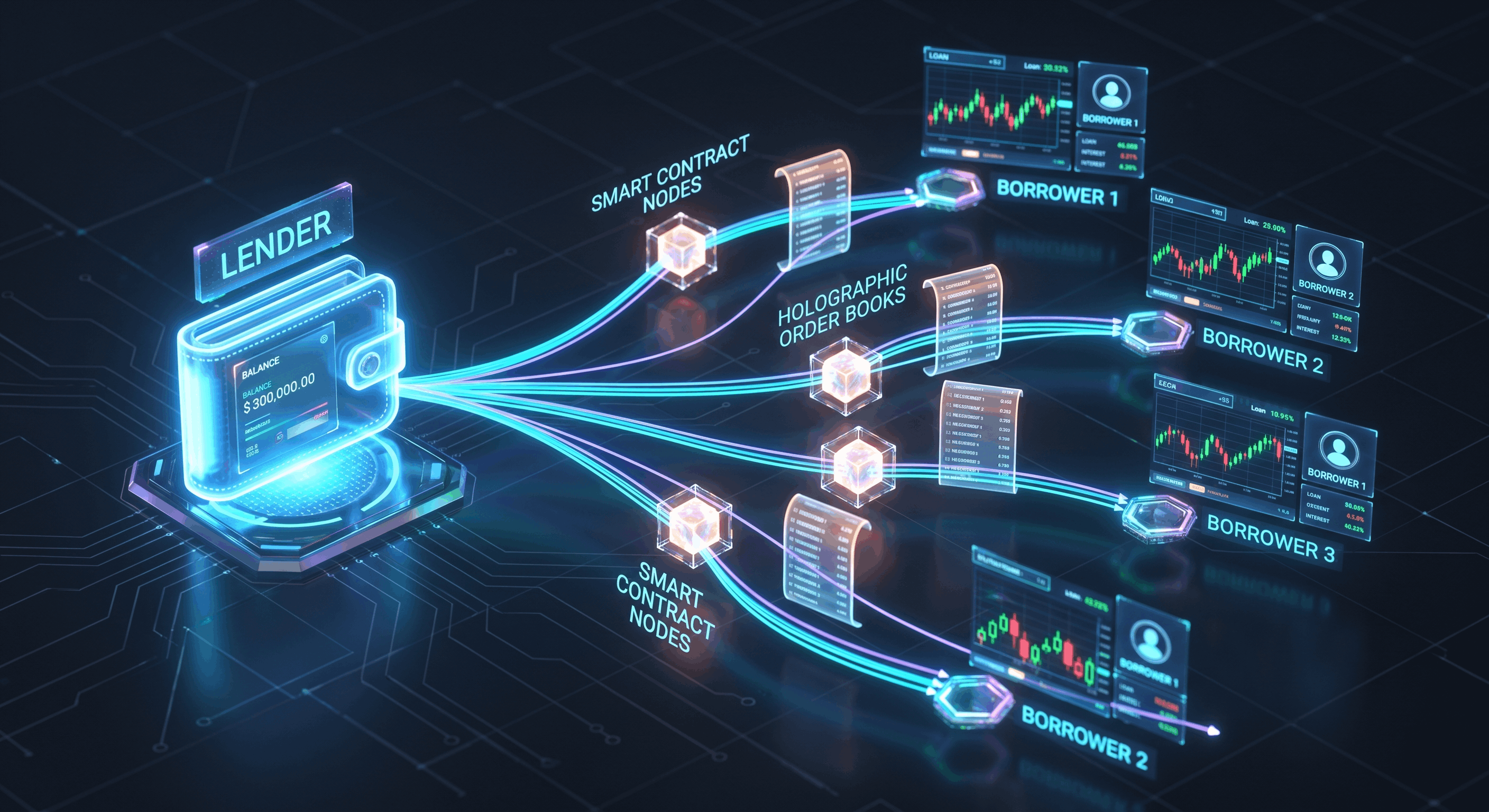

Who's on the other side? Where borrowers come from

The USD / USDT / BTC you lend goes to margin traders on Bitfinex — people who want to amplify a position (long or short) and need to borrow funds. The key point: these loans are over-collateralized. Borrowers must post collateral first, and Bitfinex's margin system force-liquidates them to repay if losses approach a threshold. So you're not lending directly to a stranger — you're lending to a system backed by collateral and enforced by the exchange. That's the fundamental reason lending risk is relatively low.

How does the funding order book work?

Like a trading order book, the funding market has two sides:

- Offers: lenders post "I'll lend N at X% for D days."

- Demand: borrowers want funds and take them from existing offers.

When a borrower comes to borrow, the system fills from the lowest-rate offers first (borrowers naturally want the cheapest money). So whether — and how fast — your offer fills depends on where your rate sits relative to the whole order book.

| Offers (rate, low to high) | Fill order |

|---|---|

| A: 8% APR, 5,000 USD | ① filled first |

| B: 10% APR, 3,000 USD | ② next |

| C: 15% APR, 2,000 USD | ③ only if demand is large enough |

| D: 30% APR, 1,000 USD | usually sits idle, unfilled |

If a borrower only wants 6,000 USD: A fills entirely + B fills 1,000 — C and D don't fill at all. A 30% APR offer looks high, but if no one borrows it, your actual earnings are 0. A high nominal rate ≠ more earnings; only filled offers count.

FRR's role in matching

Besides setting your own rate, you can post an FRR (Flash Return Rate, floating-rate) offer. FRR is Bitfinex's calculated market-average floating rate; posting at FRR means "I accept the current market floating rate, fill me with priority." FRR offers have their own priority in matching — good for people who want "guaranteed to get lent out, no need to watch the screen," at the cost of a rate that floats with the market and may dip below a manual offer in quiet conditions. To go deeper, read this complete FRR explainer.

What happens after it's lent? Term and recovery

Once matched, it becomes a fixed-term loan: the borrower pays you interest over the agreed number of days (Bitfinex funding runs 2–120 days). During that period the money is locked and can't be moved; at maturity the principal plus interest returns to your wallet and you can lend it out again. Bitfinex takes a funding fee on the interest you earn (about 15%, on interest only — never on principal). So "how many days" is also strategy: short terms are flexible but need frequent re-posting; long terms are hands-off but lock you into a low rate if market rates rise.

Why does this mechanism need a bot?

Understand the matching and you understand a bot's value: rates are dynamic — as demand shifts, the sweet spot ("fills, yet doesn't underearn") moves. A manual lender either offers too high (idle) or too low (underearns), and can't out-react someone watching 24/7. Lending bots (EarnUSD, Cryptolend, Altinvest, Coinlend, etc.) continuously watch the order book, auto-cancel and re-post, and pin your rate at the optimal spot.

But bots differ from one another, and the key is reaction speed. Most bots check on a fixed cycle (a sweep every few minutes). EarnUSD, on top of its regular 5-minute check, adds a layer of 1-minute high-rate detection: the moment a rate spike appears in the order book (usually a large borrow demand surging in), the system immediately triggers an out-of-cycle grab, placing your funds before the rate falls back. High rates often flash for only a few minutes — whoever posts first earns it — and this "second-level high-rate grabbing" is something fixed-cycle bots can't do.

Bottom line

Bitfinex lending is a rate-priority P2P order book: borrowers fill from the cheapest offers first, and your rate determines fill speed and return. Too high = idle, too low = underearn, and the sweet spot moves with the market — which is exactly why an automated bot beats manual lending, and why reaction speed (like EarnUSD's 1-minute grab) is what separates one bot from another.