Bottom line: to earn passive yield on USDT, CeFi lending (like Bitfinex funding) and DeFi (like Aave lending or Lido liquid staking) are two paths with completely different risk profiles. The difference isn't "who pays more" (both float) — it's whether you take smart-contract risk or exchange risk, how steep the learning curve is, and whose hands your money is in. This guide uses a table to help you choose.

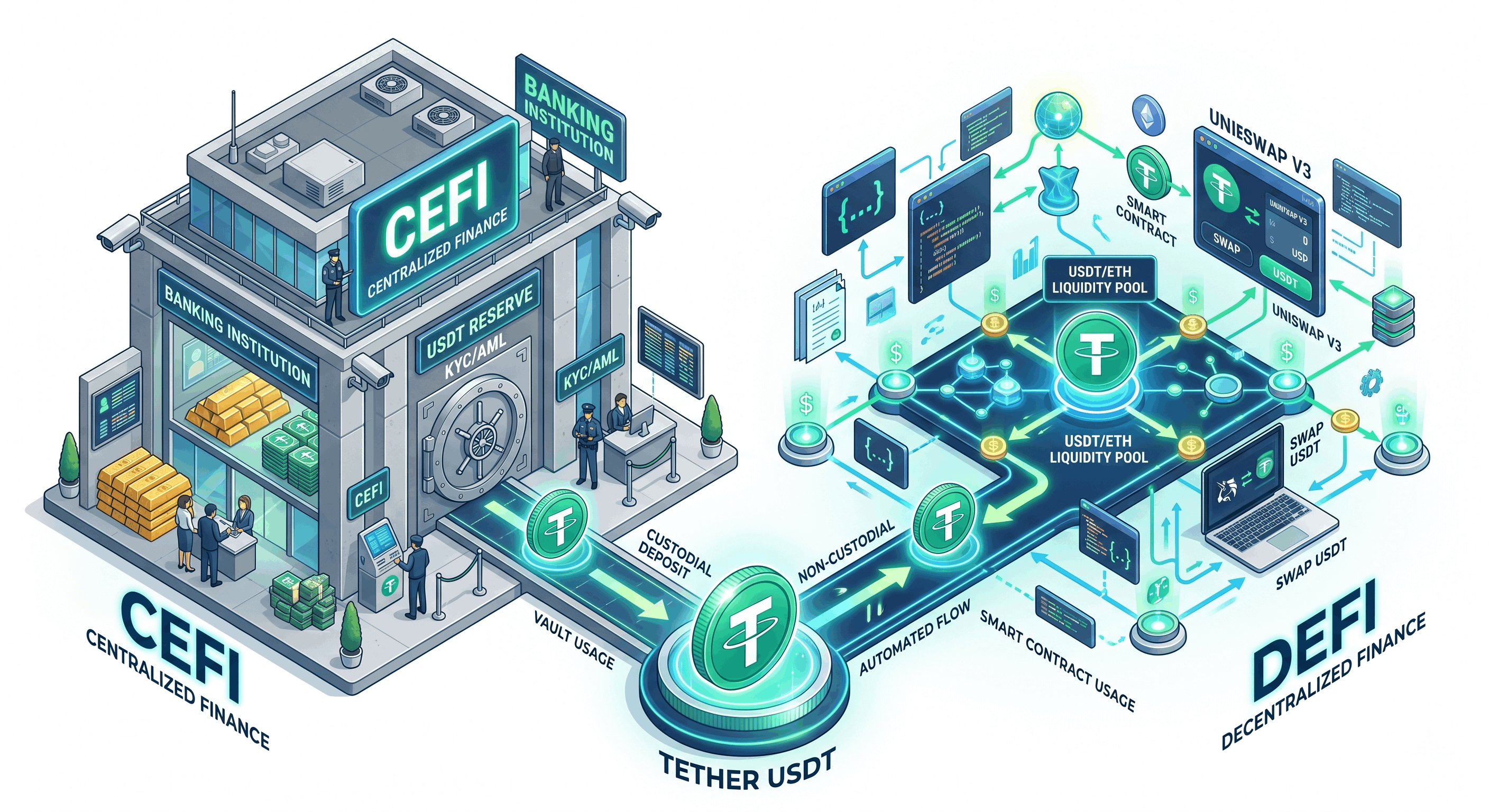

Two paths to "USDT yield"

Broadly two categories:

- CeFi lending: on a centralized exchange's funding market (e.g. Bitfinex), lend your USDT to leveraged traders for interest.

- DeFi: deposit USDT into on-chain smart-contract protocols — e.g. Aave (a lending pool) for borrow interest, or move into liquid-staking derivatives like Lido to indirectly earn staking rewards.

Bitfinex lending (CeFi P2P funding)

- Yield source: interest paid by leveraged traders, floating with supply and demand (see FRR).

- Where your money sits: in your own exchange account. With a non-custodial lending tool (lend-only, no-withdrawal API), your principal never leaves your Bitfinex account.

- Main risk: exchange risk (platform security/operations). No smart-contract-hack risk.

- Barrier: no on-chain ops, no gas, no wallet-key management. More intuitive for most people.

DeFi lending / staking (Aave, Lido, etc.)

- Yield source: Aave is interest paid by borrowers (algorithmically priced); Lido is Ethereum staking rewards (via a liquid-staking derivative).

- Where your money sits: in on-chain smart contracts, controlled by your wallet keys. You hold the keys, but the assets are exposed to contract risk.

- Main risk: smart-contract bugs/hacks, oracle/liquidation-mechanism risk, and (for staking derivatives) de-peg risk. No single-exchange-failure risk, but protocol-layer risk instead.

- Barrier: you need wallets, gas, and an understanding of bridging/approvals — a higher operational and learning cost.

Comparison table

| Dimension | Bitfinex lending (CeFi) | DeFi (Aave/Lido) |

|---|---|---|

| Yield source | Leveraged-trader interest (market-floating) | Borrow interest / staking rewards (algo or protocol) |

| Where money sits | Your exchange account | On-chain contracts (your wallet keys) |

| Main risk | Exchange risk | Smart-contract / protocol risk |

| Barrier to entry | Low (no gas / wallet) | High (wallet, gas, on-chain know-how) |

| Liquidity | By lending term, at maturity | Mostly withdrawable anytime (derivatives depend on market) |

| Best for | People who want simple USDT interest | Those fluent on-chain who can manage keys and contract risk |

Key point: two kinds of "non-custodial" aren't the same

Both DeFi and CeFi lending bots say "non-custodial," but they mean different things:

- DeFi non-custodial = you hold the keys, assets in your wallet, but exposed to smart-contract risk (if the contract is hacked, you can't get it back either).

- Bitfinex lending bot non-custodial (like EarnUSD) = principal in your own exchange account, the bot only uses a lend-only, no-withdrawal API to post offers and can't move your money; no smart-contract-hack layer, but there is exchange risk.

Neither is "absolutely safe" — just different risk profiles. It comes down to whether you can stomach contract risk or exchange risk, and whether you want to learn on-chain ops. For how to set up the API key safely, see this guide.

Which fits you?

If you're already fluent in DeFi, can manage wallet keys, and understand contract risk, DeFi gives you more options and composability. If you just want simple USDT interest without learning gas/wallets/bridging, and don't want to watch rates, lending on an exchange is usually easier — and high-rate spikes are fleeting, hard to catch by hand. EarnUSD monitors every minute, auto-grabs high rates, auto-reinvests, all non-custodial, principal staying in your own Bitfinex account.

Conclusion

Bitfinex lending vs DeFi isn't a "who pays more" contest (both float) — it's a choice of "which risk you take and how much operational cost you'll pay." CeFi lending is low-barrier with exchange-layer risk; DeFi is flexible with contract-layer risk. If you want to start simply with USDT without watching the screen, a lending bot is the pragmatic option.